Ever looked at your bank balance and wondered, “Where did all my money go?” You’re not alone. Most people don’t struggle because they never earn enough — they struggle because they mix up needs and wants without realizing it.

That daily food delivery, the “limited-time” sale, the upgraded phone you didn’t really need… it adds up fast.

Understanding Needs vs Wants is one of the simplest but most powerful money habits you can build. Once you learn the difference, budgeting gets easier, saving feels less stressful, and you stop feeling guilty every time you spend money.

Table of Contents

What Are Needs vs Wants?

At the most basic level:

- Needs are things you must have to live and function properly.

- Wants are things that improve comfort, enjoyment, or lifestyle but aren’t essential.

Sounds simple, right? The tricky part is that modern life often blurs the line.

Examples of Needs

These are usually necessary expenses:

- Rent or mortgage

- Basic groceries

- Utilities

- Healthcare

- Transportation for work

- Insurance

Examples of Wants

These are optional lifestyle choices:

- Streaming subscriptions

- Designer clothes

- Expensive gadgets

- Dining out frequently

- Luxury vacations

- Premium car upgrades

A smartphone may be a need today for communication and work. But buying the newest flagship model every year? That’s probably a want.

That distinction matters more than people think.

Why Understanding Needs vs Wants Matters

Here’s what most people don’t realize: financial stress often comes from spending on wants before covering real priorities.

When you separate needs from wants, you:

- Gain better control over your money

- Reduce impulse spending

- Build savings faster

- Avoid unnecessary debt

- Make smarter financial decisions

This is also a core part of good financial habits discussed in this guide on personal finance basics.

Even the Consumer Financial Protection Bureau recommends budgeting around essential expenses first before discretionary spending.

How to Identify Needs vs Wants in Real Life

This is where things get personal.

Sometimes a purchase can be both a need and a want depending on the situation.

For example:

| Item | Need or Want? |

|---|---|

| Basic laptop for work | Need |

| High-end gaming laptop | Want |

| Homemade meals | Need |

| Daily restaurant dining | Want |

| Reliable car | Need |

| Luxury sports car | Want |

A good trick is to ask yourself:

“Can I live without this right now?”

If the answer is yes, it’s probably a want.

Another helpful question:

“Will this still matter to me next month?”

Impulse purchases usually fail this test.

Common Mistakes People Make

Treating Every Desire Like a Need

Marketing is designed to make wants feel urgent. Companies constantly tell you that you “deserve” upgrades.

You probably don’t need most of them.

Emotional Spending

Stress, boredom, and even happiness can trigger spending.

A bad day turns into online shopping. A good day becomes a celebration purchase.

It happens to everyone sometimes, but repeated emotional spending hurts long-term financial stability.

Ignoring Small Purchases

People often focus on large expenses while ignoring smaller daily habits.

A ₹250 coffee every workday may not seem serious, but over a year, it becomes a surprisingly large amount.

According to Investopedia’s budgeting guide, tracking recurring discretionary spending is one of the fastest ways to improve personal finances.

Practical Tips to Control Your Money Better

Create a Simple Budget

You don’t need complicated spreadsheets.

Start with three categories:

- Essentials (needs)

- Lifestyle spending (wants)

- Savings

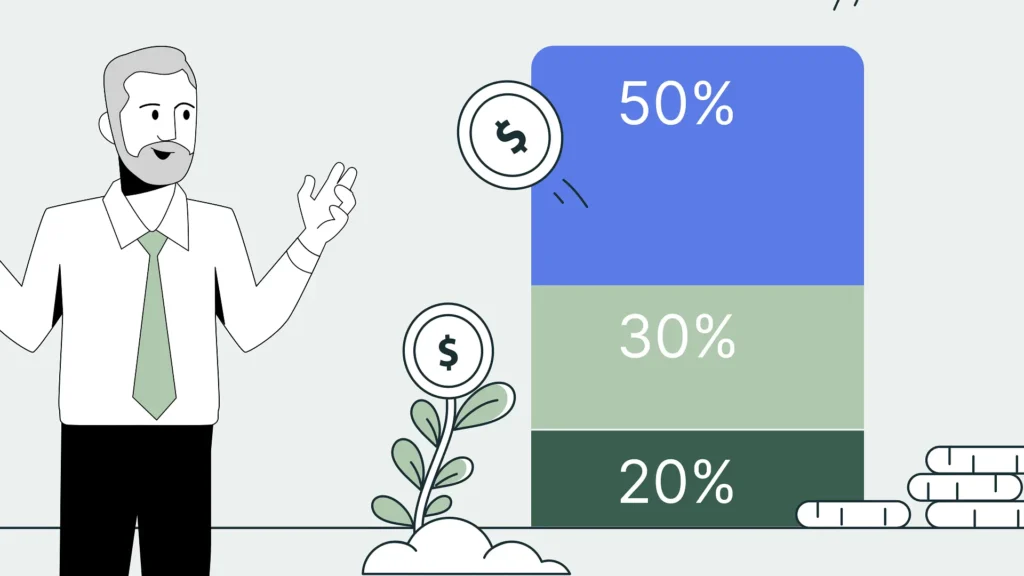

Many beginners use the 50/30/20 rule:

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

Pause Before Buying

Try the 24-hour rule for non-essential purchases.

If you still want the item after a day, think about it again carefully.

Most impulse spending disappears with time.

Set Financial Goals

Saving becomes easier when you know why you’re doing it.

Examples include:

- Emergency fund

- Travel savings

- Paying off debt

- Buying a home

- Early retirement

Having goals helps you prioritize needs over temporary wants.

You can also learn more about long-term money management in this article on why financial planning matters.

Use Cash or Spending Limits

People tend to spend less when they physically see money leaving their hands.

If overspending is a problem, try:

- Weekly spending limits

- Separate savings accounts

- Cash-only budgets for entertainment

Even small boundaries can make a huge difference.

Needs vs Wants and Social Media

Let’s be honest — social media makes comparison worse.

You see influencers traveling constantly, buying expensive products, and living luxurious lifestyles. But what you don’t see is the debt, sponsorships, or financial reality behind the scenes.

Trying to match someone else’s lifestyle can quietly destroy your budget.

A better approach is focusing on your own priorities and financial goals instead of online pressure.

FAQs

What is the difference between needs and wants?

Needs are essential for survival and daily living, while wants are optional things that improve comfort or enjoyment.

Can something be both a need and a want?

Yes. A phone may be a need, but choosing an expensive premium model becomes a want.

Why is understanding Needs vs Wants important?

It helps you budget better, reduce unnecessary spending, and save more money over time.

How can I stop impulse spending?

Use waiting periods, set budgets, avoid emotional shopping, and track your expenses regularly.

Is entertainment considered a want?

Usually yes, although moderate entertainment spending can still be part of a healthy budget.

Conclusion

Understanding Needs vs Wants isn’t about removing all fun from your life. You don’t have to stop enjoying coffee, vacations, or hobbies.

The goal is balance.

When you recognize the difference between essential spending and lifestyle spending, you start making smarter choices automatically. Over time, those choices lead to less stress, more savings, and better financial freedom.

Start small. Review your last few purchases honestly and ask yourself: “Was this truly a need, or just a want in the moment?”

That one habit alone can completely change how you manage money.