Let’s be honest—most of us weren’t taught how to manage money properly.

You probably learned algebra in school, but nobody explained credit scores, budgeting, taxes, or why some people always seem financially stressed even with decent salaries. That’s where personal finance comes in.

If you’ve ever wondered why your paycheck disappears so quickly, how people save for houses, or what investing actually means, you’re already thinking about personal finance without realizing it.

At its core, personal finance is simply the way you manage your money. That includes earning, spending, saving, investing, and planning for the future. It sounds straightforward, but small financial decisions made consistently over time can completely change your life.

The good news? You don’t need to be rich, a finance graduate, or a stock market expert to get better with money. You just need a few solid habits and a basic understanding of how money works.

Table of Contents

What Is Personal Finance?

Personal finance refers to how individuals manage their financial activities, including:

- Budgeting

- Saving money

- Investing

- Managing debt

- Retirement planning

- Insurance

- Tax planning

In simple words, it’s the process of making smart decisions with your money so you can live comfortably today while preparing for the future.

Think of personal finance like fitness.

You don’t become healthy after one workout, and you don’t become financially secure after one paycheck. What matters is consistency over time.

Someone earning ₹40,000 per month with good financial habits may end up wealthier than someone earning ₹2 lakh but spending recklessly.

That’s the power of personal finance.

Why Personal Finance Matters

Here’s what most people don’t realize: money problems usually create stress long before they create actual financial disasters.

Living paycheck to paycheck, carrying debt, or having zero emergency savings can quietly affect your mental health, relationships, and long-term goals.

Good personal finance helps you:

- Reduce financial stress

- Build savings for emergencies

- Avoid unnecessary debt

- Achieve life goals faster

- Prepare for retirement

- Gain financial independence

According to the Consumer Financial Protection Bureau, even basic budgeting and saving habits can significantly improve financial stability over time.

Money may not buy happiness, but financial security definitely buys peace of mind.

The 5 Main Areas of Personal Finance

1. Income

Everything starts with income.

Your income is the money you earn from sources like:

- Salary or wages

- Freelancing

- Business income

- Investments

- Side hustles

- Rental income

The goal isn’t only to earn more money—it’s also to manage it wisely.

A lot of beginners focus entirely on increasing income while ignoring spending habits. That’s why some high earners still struggle financially.

Practical Tip

Try tracking every source of income for one month. Many people underestimate how much irregular income or small side earnings add up over time.

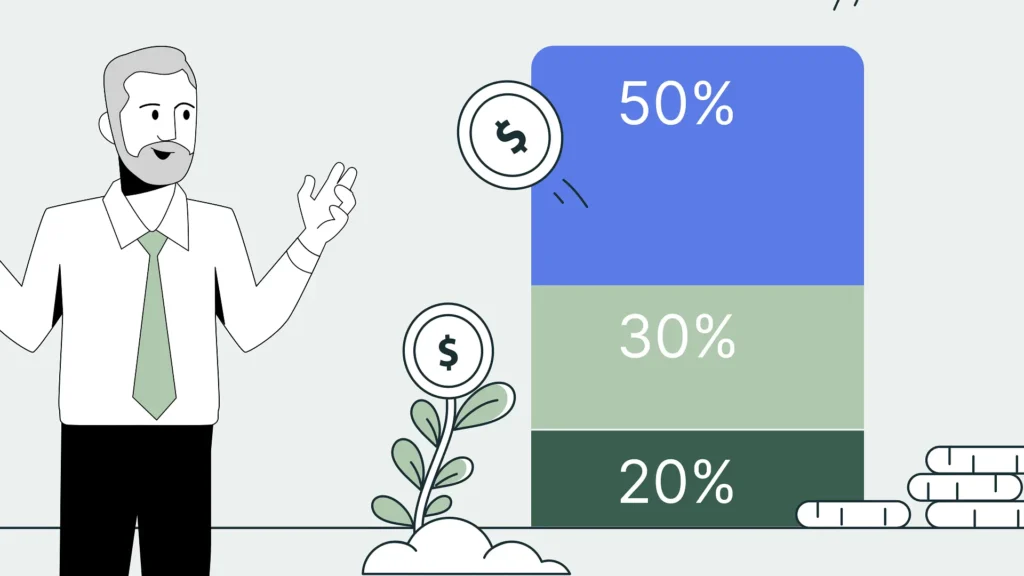

2. Budgeting

Budgeting is the foundation of personal finance.

A budget simply tells your money where to go instead of wondering where it went.

And no, budgeting doesn’t mean you can never enjoy life. It just means spending intentionally.

A Simple Beginner Budget

One popular method is the 50/30/20 rule:

- 50% for needs (rent, groceries, bills)

- 30% for wants (entertainment, eating out)

- 20% for savings and investments

For example, if you earn ₹50,000 monthly:

- ₹25,000 → necessities

- ₹15,000 → lifestyle spending

- ₹10,000 → savings/investing

This approach keeps spending balanced without feeling restrictive.

The U.S. Securities and Exchange Commission’s investor education portal also recommends budgeting as a core financial habit for beginners.

Common Budgeting Mistakes

Ignoring Small Expenses

Daily coffee, food delivery, and subscriptions may seem harmless individually, but together they can drain thousands every month.

Making Unrealistic Budgets

People often create strict budgets they can’t maintain. If your budget feels miserable, you probably won’t stick with it.

Not Tracking Spending

You can’t improve what you don’t track.

Even a simple notes app can help.

3. Saving Money

Saving gives you financial breathing room.

Without savings, even a small emergency—like a medical bill or car repair—can turn into debt.

Start With an Emergency Fund

An emergency fund is money set aside for unexpected expenses.

Most experts recommend saving:

- 3–6 months of living expenses

If that sounds overwhelming, start smaller.

Even ₹5,000 or ₹10,000 saved consistently is better than nothing.

Easy Ways to Save More

Automate Savings

Set automatic transfers to a savings account after every paycheck.

Reduce Lifestyle Inflation

When income increases, people often upgrade everything immediately. Try increasing savings before increasing spending.

Use Separate Accounts

Keeping savings separate from spending money reduces temptation.

4. Managing Debt

Debt itself isn’t always bad.

A home loan or education loan can sometimes help improve your future earning potential. The real danger comes from high-interest debt, especially credit cards.

Good Debt vs Bad Debt

| Good Debt | Bad Debt |

|---|---|

| Education loan | Credit card debt |

| Business loan | Impulse purchases |

| Home loan | Buy-now-pay-later misuse |

How to Pay Off Debt Faster

Debt Snowball Method

Pay off the smallest debt first while making minimum payments on others.

This creates psychological momentum.

Debt Avalanche Method

Focus on the highest-interest debt first to save more money long term.

Important Reminder

Missing loan payments regularly can damage your credit score, which affects future borrowing ability.

You can learn more about credit management through Experian’s official credit education resources.

5. Investing

Saving protects money.

Investing helps grow it.

That’s one of the biggest differences beginners need to understand.

If your money only sits in a regular savings account, inflation slowly reduces its purchasing power over time.

Investing allows your money to potentially grow faster.

Common Investment Options

Stocks

Buying shares of companies.

Higher risk, but potentially higher returns.

Mutual Funds

Professionally managed investment funds that pool money from many investors.

Great for beginners.

ETFs (Exchange-Traded Funds)

Low-cost funds traded like stocks.

Fixed Deposits and Bonds

Safer investments with lower returns.

The Power of Compound Growth

Here’s a simple example:

If you invest ₹5,000 monthly with average annual growth of 12%, you could potentially build a substantial amount over decades—even without becoming a high earner.

Time matters more than timing.

Starting early is one of the biggest advantages in investing.

Personal Finance and Financial Goals

Money management becomes easier when tied to real goals.

Without goals, saving often feels pointless.

Short-Term Goals

- Buying a phone

- Vacation fund

- Emergency savings

Medium-Term Goals

- Buying a car

- Paying off debt

- Starting a business

Long-Term Goals

- Retirement

- Buying a house

- Financial independence

Clear goals help you stay motivated during difficult financial periods.

Common Personal Finance Mistakes Beginners Make

Living Beyond Your Means

Social media makes overspending feel normal.

People often finance lifestyles they can’t actually afford.

Ignoring Emergency Savings

Many beginners start investing aggressively before building basic savings.

That can backfire quickly during emergencies.

Depending Entirely on One Income Source

One job is good.

Multiple income streams are safer.

Waiting Too Long to Invest

A lot of people think investing is only for wealthy individuals.

In reality, small consistent investments matter more than large occasional ones.

Not Learning About Money

Financial literacy is one of the highest-return skills you can build.

Even spending 15 minutes daily learning about money can make a huge difference over time.

Simple Personal Finance Tips for Beginners

If you’re just getting started, keep things simple.

You don’t need complicated spreadsheets or advanced investing strategies immediately.

Start Tracking Expenses

Awareness changes behavior.

Track spending for one month without judgment.

Follow a Basic Budget

Use whatever system feels realistic and sustainable.

Build an Emergency Fund First

Before aggressive investing, create financial stability.

Avoid High-Interest Debt

Credit card interest can destroy financial progress surprisingly fast.

Invest Consistently

Small monthly investments matter more than trying to “get rich quick.”

Learn Continuously

Read books, listen to finance podcasts, and follow trusted financial resources.

The Financial Literacy and Education Commission offers free educational resources for improving money management skills.

How Personal Finance Improves Your Life

People often think personal finance is only about becoming rich.

It’s actually more about creating freedom.

Good money management can help you:

- Quit a toxic job

- Handle emergencies calmly

- Sleep better at night

- Support your family

- Travel without guilt

- Retire comfortably

Financial stability creates options.

And options create freedom.

That’s why learning personal finance early matters so much.

FAQs About Personal Finance

What is personal finance in simple words?

Personal finance is the process of managing your money through budgeting, saving, investing, and controlling expenses.

Why is personal finance important?

It helps reduce financial stress, build savings, avoid debt, and prepare for future goals like retirement or buying a home.

How can beginners start personal finance?

Start by:

Tracking expenses

Creating a simple budget

Building emergency savings

Paying off high-interest debt

Learning basic investing

What are the main areas of personal finance?

The main areas include:

Income

Budgeting

Saving

Investing

Debt management

Financial planning

Is investing necessary in personal finance?

Yes. Saving alone may not beat inflation over time. Investing helps grow wealth and build long-term financial security.

Conclusion

So, what is personal finance?

It’s not about being perfect with money. It’s about becoming more intentional with it.

You don’t need to master investing overnight or create a flawless budget tomorrow morning. Even small improvements—tracking expenses, saving regularly, or learning about investing—can completely change your financial future over time.

The important thing is starting.

Because once you understand how personal finance works, money stops feeling confusing and starts becoming a tool you can actually control.

And honestly, that feeling is worth a lot.