Let’s be honest—most people know they should budget, but actually sitting down and creating one feels overwhelming. You might wonder where to start, what to include, or whether budgeting means giving up everything you enjoy.

The good news? It doesn’t have to be complicated.

A monthly budget is simply a plan for your money. It tells every dollar where to go before you spend it. Whether you’re trying to save for a vacation, pay off debt, build an emergency fund, or just stop wondering where your paycheck disappeared, learning how to create a monthly budget is one of the most valuable financial skills you can develop.

If you’ve ever asked yourself, “How do I create a budget?” or “How can I create a personal budget that actually works?” this guide will walk you through the process step by step.

Table of Contents

Why Creating a Monthly Budget Matters

Many people think budgeting is restrictive. In reality, it’s the opposite.

A good budget gives you freedom because you’re making intentional decisions about your money instead of reacting to expenses as they appear.

Benefits of having a monthly budget include:

- Better control over spending

- Reduced financial stress

- More consistent savings

- Faster debt repayment

- Improved financial decision-making

- Greater confidence about the future

In fact, understanding budgeting is a key part of effective financial management. If you’re new to personal finance, check out our guide on what personal finance really means.

How to Create a Monthly Budget: Step-by-Step

Step 1: Calculate Your Monthly Income

Before planning your spending, you need to know exactly how much money comes in each month.

Include:

- Salary after taxes

- Freelance income

- Side hustle earnings

- Rental income

- Other regular sources of income

For example:

| Income Source | Amount |

|---|---|

| Salary | $3,500 |

| Freelance Work | $500 |

| Total Income | $4,000 |

If your income varies each month, use the average from the last 6–12 months.

Step 2: Track Your Expenses

Here’s what most people don’t realize: budgeting often fails because they underestimate their spending.

Review:

- Bank statements

- Credit card statements

- Digital wallet transactions

- Subscription services

Write down every expense, even the small ones.

Common categories include:

Fixed Expenses

These usually stay the same each month:

- Rent or mortgage

- Insurance

- Internet

- Loan payments

- Phone bills

Variable Expenses

These change from month to month:

- Groceries

- Dining out

- Fuel

- Entertainment

- Shopping

Many people are surprised by how much they spend on convenience purchases and impulse buys.

Step 3: Separate Needs from Wants

One of the biggest budgeting breakthroughs comes from understanding the difference between necessities and optional spending.

Needs include:

- Housing

- Utilities

- Food

- Transportation

- Healthcare

Wants include:

- Streaming subscriptions

- Premium memberships

- Designer clothing

- Frequent takeout meals

If you’re unsure where to draw the line, our guide on needs vs wants and controlling your money better can help clarify the difference.

Step 4: Set Financial Goals

A budget without goals is just a spreadsheet.

Ask yourself:

- Do I want an emergency fund?

- Am I paying off debt?

- Am I saving for a home?

- Do I want to invest more?

Short-term goals might include:

- Saving $1,000 for emergencies

- Paying off a credit card

Long-term goals could be:

- Buying a house

- Retirement planning

- Building investment wealth

The Consumer Financial Protection Bureau recommends setting clear and measurable financial goals to stay motivated.

Step 5: Choose a Budgeting Method

There isn’t one perfect budget for everyone.

Here are three popular approaches.

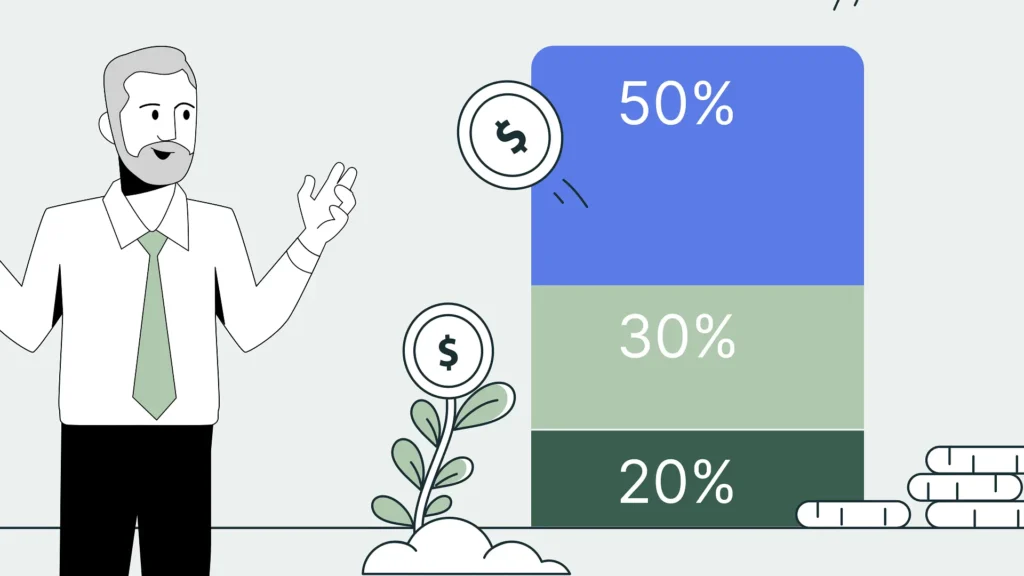

50/30/20 Budget

Allocate:

- 50% to needs

- 30% to wants

- 20% to savings and debt repayment

Example with $4,000 income:

- Needs: $2,000

- Wants: $1,200

- Savings/Debt: $800

Zero-Based Budget

Every dollar receives a specific purpose.

Income minus expenses equals zero—not because you’re broke, but because every dollar has been assigned.

Pay Yourself First

Save first, spend second.

Many successful savers automatically transfer money into savings on payday before paying for anything else.

Step 6: Create Your Budget Plan

Now it’s time to put everything together.

Example monthly budget:

| Category | Budget |

|---|---|

| Housing | $1,200 |

| Utilities | $200 |

| Groceries | $400 |

| Transportation | $250 |

| Entertainment | $200 |

| Savings | $800 |

| Miscellaneous | $250 |

| Total | $3,300 |

Adjust according to your situation.

Remember, your budget should fit your life—not someone else’s.

Step 7: Monitor and Adjust Monthly

Your first budget won’t be perfect.

That’s normal.

Treat the first few months as an experiment.

Review:

- What categories exceeded expectations?

- Where did you save money?

- Which expenses were forgotten?

The most successful budgeters review their finances regularly instead of creating a budget once and forgetting about it.

Practical Tips to Make Budgeting Easier

Automate Savings

Automatic transfers remove the temptation to spend.

Use Budgeting Apps

Apps can simplify tracking and reporting.

- Mint alternatives

- YNAB

- EveryDollar

- PocketGuard

Build an Emergency Fund

According to the Federal Deposit Insurance Corporation (FDIC), having emergency savings helps protect against unexpected financial setbacks.

Aim for:

- 3–6 months of essential expenses

- Start small if necessary

Review Subscriptions Regularly

Many people pay for services they barely use.

A quick subscription audit can free up money immediately.

Common Budgeting Mistakes to Avoid

Being Too Restrictive

If you eliminate all fun spending, you’ll likely quit.

Include room for enjoyment.

Forgetting Irregular Expenses

Examples:

- Car repairs

- Annual subscriptions

- Holiday gifts

- Medical expenses

Not Tracking Spending

A budget only works when you compare it against reality.

Giving Up After One Bad Month

Unexpected expenses happen.

The key is consistency, not perfection.

You can also avoid several beginner pitfalls by reading about common money mistakes people make when starting their financial journey.

How to Create a Personal Budget That Fits Your Lifestyle

A personal budget should reflect your priorities.

Someone saving for a home may allocate more money to savings.

A young professional paying off student loans may focus on debt reduction.

A growing family may prioritize childcare and household expenses.

The best budget isn’t the strictest one—it’s the one you’ll actually follow.

Strong budgeting habits also support long-term financial success. That’s why understanding the importance of financial planning for your future can help you stay committed to your goals.

Frequently Asked Questions

How do I create a budget if my income changes every month?

Use your average income from the last six to twelve months and base your budget on the lower end of that average.

How much should I save each month?

A common recommendation is at least 20% of your income, but any consistent amount is better than none.

What’s the easiest budgeting method for beginners?

The 50/30/20 budget is often the simplest because it’s easy to understand and implement.

Should I budget every expense?

Yes. Even small expenses add up over time and can affect your financial goals.

How often should I review my budget?

Review your budget weekly and make larger adjustments at the end of each month.

Conclusion

Learning how to create a monthly budget doesn’t require complicated spreadsheets or financial expertise. It starts with understanding your income, tracking your expenses, setting realistic goals, and making intentional decisions with your money.

The most important thing to remember is that budgeting is a skill. Like any skill, it gets easier with practice.

Start simple. Track your spending. Make adjustments as you go.

A year from now, you’ll likely be glad you took the time to build a budget that works for your life and financial goals.

If you’ve been wondering how to create a monthly budget or how to create a personal budget that actually sticks, there’s no better time to start than today.