Let’s be honest—budgeting often sounds a lot harder than it actually needs to be.

Many people start with good intentions, download a budgeting app, create a spreadsheet, and then abandon the whole thing a few weeks later because it feels too complicated. If you’ve ever felt that way, you’re not alone.

That’s exactly why the 50/30/20 rule has become one of the most popular budgeting methods in personal finance. Instead of tracking every single dollar, this approach gives you a simple framework for managing your income, covering your expenses, and building savings without feeling overwhelmed.

Whether you’re just starting your financial journey or looking for a more practical way to manage your money, the 50/30/20 rule can help you create a balanced budget that actually fits real life.

Before diving into the details, it helps to understand the basics of money management and how it fits into your overall financial picture. Our guide on personal finance for beginners provides a great foundation.

Table of Contents

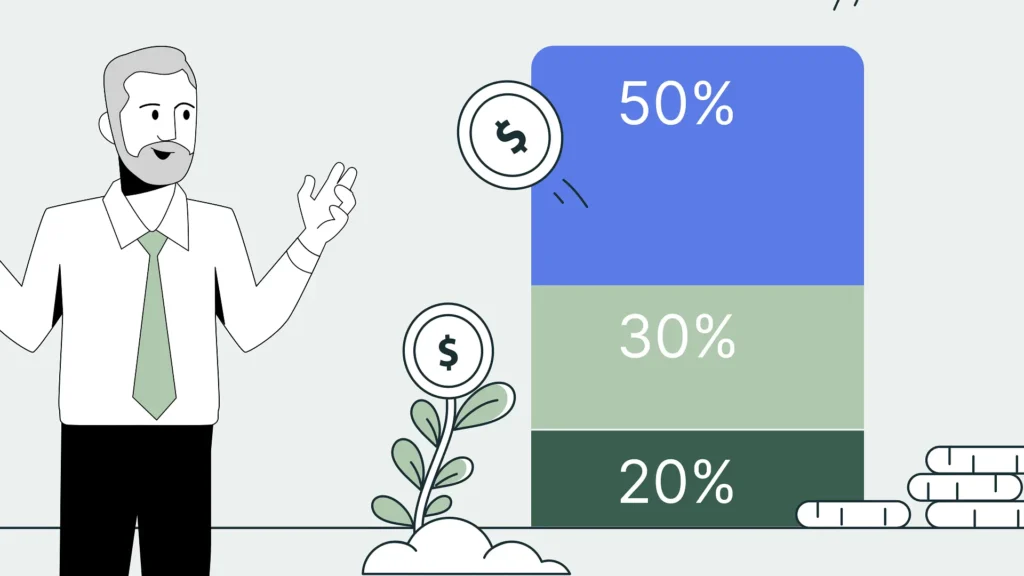

What Is the 50/30/20 Rule?

The 50/30/20 rule is a simple budgeting method that divides your after-tax income into three categories:

- 50% for Needs

- 30% for Wants

- 20% for Savings and Debt Repayment

The concept became widely known after being popularized by U.S. Senator and bankruptcy expert Elizabeth Warren in her book All Your Worth: The Ultimate Lifetime Money Plan.

The idea is straightforward: instead of tracking dozens of spending categories, you focus on three broad areas that cover most financial decisions.

Here’s what a typical 50/30/20 budget looks like:

| Category | Percentage |

|---|---|

| Needs | 50% |

| Wants | 30% |

| Savings & Debt Repayment | 20% |

This simple structure makes budgeting easier while still helping you maintain healthy financial habits.

How the 50/30/20 Budget Works

Let’s say your monthly take-home pay is $4,000.

Using the 50/30/20 budget, your money would be divided like this:

- Needs: $2,000

- Wants: $1,200

- Savings and debt repayment: $800

Rather than worrying about every small expense, you focus on keeping your overall spending within these percentages.

Let’s break down each category.

50% for Needs

What Counts as a Need?

Needs are essential expenses—the things you must pay to maintain your basic standard of living.

Examples include:

- Rent or mortgage payments

- Utilities

- Groceries

- Transportation

- Health insurance

- Childcare

- Minimum debt payments

A useful question to ask is:

“Could I reasonably live without this?”

If the answer is no, it’s probably a need.

Common Mistake

Many people accidentally classify lifestyle expenses as needs.

For example:

- Premium streaming subscriptions

- Daily coffee shop visits

- Luxury gym memberships

These may feel essential, but they’re typically wants rather than needs.

If you’re unsure where to draw the line, our guide on needs vs wants can help clarify the difference.

30% for Wants

What Counts as a Want?

Wants are the things that make life more enjoyable but aren’t necessary for survival.

Examples include:

- Dining out

- Entertainment

- Vacations

- Streaming services

- Hobbies

- Shopping

- Upgraded electronics

This category often gets misunderstood.

The 50/30/20 rule doesn’t tell you to stop enjoying life. Instead, it creates room for fun spending while keeping it under control.

That’s one reason the system works so well—it feels realistic.

Many strict budgets fail because they remove all enjoyment from spending. The 50 30 20 budget recognizes that financial success shouldn’t mean living miserably.

20% for Savings and Debt Repayment

The Most Powerful Category

The final 20% goes toward improving your financial future.

This portion can be used for:

- Emergency fund contributions

- Retirement savings

- Investment accounts

- Extra debt payments

- Saving for major goals

- Building wealth

This is where the 50/30/20 savings rule really shines.

Even small, consistent contributions can grow significantly over time.

For example:

Saving $500 per month may not seem life-changing today.

But over 10 years, that’s $60,000 saved before accounting for any investment growth.

That’s the power of consistency.

For guidance on creating long-term financial goals, the Consumer Financial Protection Bureau offers several helpful budgeting and savings resources.

Why the 50/30/20 Rule Works So Well

1. It’s Easy to Understand

You don’t need advanced spreadsheets.

You don’t need accounting knowledge.

You simply divide your income into three categories.

2. It Reduces Budgeting Stress

Tracking every expense can become exhausting.

The 50/30/20 rule focuses on the bigger picture instead.

3. It Encourages Saving

Many people save whatever money is left over at the end of the month.

The problem?

Often, nothing is left.

The 50/30/20 savings rule flips the process by making saving a priority.

4. It’s Flexible

Life changes.

Income changes.

Expenses change.

The framework can adapt without requiring a complete budget overhaul.

How to Start Using the 50/30/20 Rule

Step 1: Calculate Your After-Tax Income

Use your take-home pay rather than your gross salary.

This is the amount that actually reaches your bank account.

Step 2: Review Current Spending

Look at the past two or three months of transactions.

Identify:

- Essential expenses

- Lifestyle spending

- Savings contributions

Step 3: Compare Your Numbers

See how closely your current spending matches the ideal percentages.

Most people discover they spend more than 50% on needs or more than 30% on wants.

That’s normal.

Step 4: Make Small Adjustments

Focus on gradual improvements.

You don’t need perfection on day one.

Step 5: Track Progress Monthly

Review your spending each month and adjust as needed.

If you’re building a budget from scratch, check out our guide on creating a monthly budget for additional tips.

Real-Life Example of the 50/30/20 Rule

Imagine Sarah earns $3,500 per month after taxes.

Her ideal allocation would be:

Needs (50%)

- Rent: $1,000

- Utilities: $150

- Groceries: $300

- Transportation: $200

- Insurance: $100

Total: $1,750

Wants (30%)

- Dining out

- Entertainment

- Shopping

- Streaming subscriptions

Total: $1,050

Savings (20%)

- Emergency fund: $300

- Retirement savings: $250

- Extra student loan payments: $150

Total: $700

This structure helps Sarah enjoy her income while still making meaningful financial progress.

Common Mistakes to Avoid

- Ignoring High Living Costs: Housing alone may exceed 50% of income in some areas.

- Not Tracking Spending: Regular reviews help keep your budget on track.

- Forgetting Emergency Savings: Don’t focus solely on retirement accounts.

- Giving Up Too Quickly: Budgeting is a skill that improves over time.

The FDIC recommends maintaining emergency savings to help manage unexpected financial setbacks.

You can also avoid many financial setbacks by learning from these common money mistakes beginners make.

When the 50/30/20 Rule Might Not Work

Although it’s a great starting point, it’s not perfect for everyone.

You may need adjustments if:

- You have significant debt

- Your income varies monthly

- You’re aggressively saving for a major goal

- You live in a very high-cost area

In these situations, you might temporarily shift the percentages.

- 60% Needs / 20% Wants / 20% Savings

- 50% Needs / 20% Wants / 30% Savings

The goal is progress, not perfection.

Benefits of Following the 50/30/20 Savings Rule

- Simpler budgeting

- Better spending awareness

- Reduced financial stress

- Consistent saving habits

- Improved financial discipline

- Greater long-term wealth building

Most importantly, it creates a balanced relationship with money.

You’re not depriving yourself. You’re simply giving every dollar a purpose.

Frequently Asked Questions

Is the 50/30/20 rule good for beginners?

Yes. Its simplicity makes it one of the best budgeting methods for people who are new to personal finance.

Does the 20% include debt payments?

Extra debt payments beyond minimum requirements can be included in the 20% savings category.

What if my needs exceed 50%?

Adjust the percentages based on your situation and focus on gradual improvement over time.

Can I use the 50/30/20 rule with irregular income?

Yes. Calculate percentages based on your average monthly income and update them as your earnings change.

Is the 50/30/20 budget suitable for families?

Absolutely. Many families use the framework to simplify household budgeting and financial planning.

Conclusion

The 50/30/20 rule remains one of the easiest and most effective budgeting methods available.

Instead of obsessing over every expense, it gives you a practical structure: cover your essentials, enjoy your money responsibly, and consistently invest in your future.

Whether you’re trying to build an emergency fund, pay off debt, or simply gain more control over your finances, the 50/30/20 budget offers a realistic path forward.

The best part? You don’t need to be a financial expert to start.

Take a look at your income, divide it into the three categories, and make small adjustments as needed. Over time, those small changes can lead to significant financial progress.

Start today, review your spending habits, and see how the 50/30/20 savings rule can help you budget, save, and spend smarter.